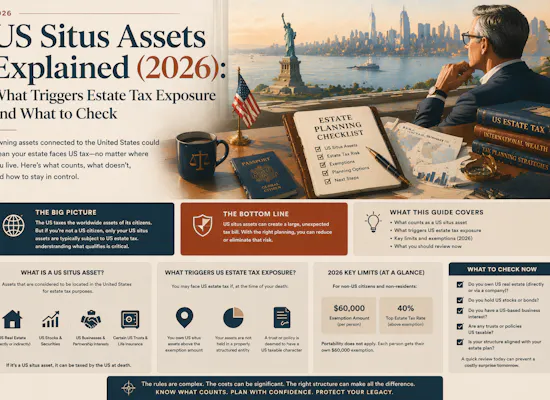

US Situs Assets Explained: What Triggers Estate Tax Exposure and What to Check

For a nonresident who is not a US citizen, US estate tax exposure is generally triggered by owning US-situated property at death, not by worldwide wealth. Common US situs assets include US real estate, tangible property physically in the US, and shares of US corporations. Some assets are generally treated as outside the US estate tax net, including certain bank deposits, certain qualifying debt obligations, and life insurance proceeds on the life of the nonresident decedent.

People also ask

- What counts as a US situs asset for estate tax?

- Do US shares trigger estate tax for non-US investors?

- Are US-domiciled ETFs subject to US estate tax for expats?

- Are bank deposits in the US caught by estate tax?

- What is Form 706-NA and when is it required?

- Does the US-UK estate tax treaty help British expats?

- How do US situs assets affect families living in the UAE?

- What should non-US families check before holding US assets?

At a glance

- For a nonresident not a citizen of the United States, the core issue is US-situated property, not worldwide wealth.

- If the fair market value at death of the decedent’s US-situated assets exceeds $60,000, the executor generally must file Form 706-NA.

- Stock of US corporations is generally US situs property, regardless of where the share certificate or brokerage account sits.

- Certain bank deposits, certain qualifying debt obligations, and life insurance proceeds on the life of a nonresident decedent are generally treated as outside the US estate tax net.

- Estate tax treaties, including those with the UK and South Africa, can materially improve the result in some cases, but they do not remove the need to classify the assets correctly first.

- The practical trap for many expats is not “being American”. It is owning the wrong US-linked asset in the wrong wrapper and leaving the problem for executors to discover after death. This is an inference from the IRS situs rules and filing framework.

What does US Situs Assets mean?

Most families do not get caught by US estate tax because they were trying to be clever.

They get caught because they bought what looked like a normal investment, held it on what looked like a normal platform, and assumed the estate-planning consequences would sort themselves out later.

That is the real problem here.

A British expat in Dubai buys US shares through an offshore broker.

A South African family owns a Florida property because it felt like a sensible diversification move.

A non-US investor holds a large position in a US-domiciled ETF and thinks, correctly, that they own a diversified fund, but misses the much more important legal question of what that fund is for estate-tax purposes.

A spouse or executor then finds out after death that the issue was never “are we American?” but “what exactly did we own?”

That is why this article matters.

For a nonresident not a citizen of the United States, the US estate-tax conversation starts with classification. Not with nationality. Not with where you live. Not with which app you use to hold the investments. Classification. The IRS position is that the tax applies to US-situated property, and the filing trigger for Form 706-NA is generally crossed once the fair market value at death of the decedent’s US-situated assets exceeds $60,000.

That is a very low threshold for globally mobile professionals.

It is also why modest-looking US exposure can turn into a much bigger estate-planning problem than people expect.

The rule that matters first

If you remember one thing from this article, make it this:

US estate tax for a nonresident non-citizen is driven by US situs assets at death.

That sounds obvious once written down, but it changes the whole analysis.

It means the right question is not:

- Do I have a US broker?

- Do I receive dividends from America?

- Do I invest in the US market?

- Am I a US citizen?

The right question is:

- Which of my assets are treated as situated in the United States for estate-tax purposes?

That is the question that drives exposure, filing, and later administration. The IRS page for nonresidents not citizens says exactly that in practical terms: the estate tax applies to property situated in the US, and if the US-situated assets exceed $60,000, the executor must generally file Form 706-NA.

This is where many expats start on the wrong footing. They hear about the very large US federal estate-tax exemptions that apply in domestic US planning and assume they have a similar buffer. Usually, they do not. For NRNC estates, the $60,000 filing threshold remains the number that matters first, and the general maximum unified credit is far smaller unless treaty relief changes the picture.

So the first decision point is brutally simple:

Would your US situs assets exceed $60,000 if you died tomorrow?

If the answer is yes, this is not a niche academic point. It is an estate-planning issue now.

What usually counts as a US situs asset

US real estate

US real estate is one of the easiest categories to understand and one of the hardest to ignore.

If a non-US person owns a property physically located in the United States, that is typically US situs property for estate-tax purposes. The same broad point applies to tangible personal property physically located in the US.

So if the family owns:

- a Florida condo

- a New York apartment

- a holiday home in California

- or tangible valuables physically in the US

that should be treated as a clear estate-tax review point.

This is one reason US property ownership so often creates problems for internationally mobile families. It feels intuitive, solid, and familiar. But from an estate-tax angle, it is also one of the least forgiving categories because the situs connection is so direct.

Shares of US corporations

This is the most common investment trap.

The IRS instructions say that stock of corporations organised in or under US law is generally property located in the United States, regardless of where the stock certificate is held. In plain English, if you are a non-US person and you directly own US shares, that can create US estate-tax exposure.

This is where a lot of people get blindsided.

They think they own “an investment account”.

The IRS asks what is inside the account.

They think they own “global equities”.

The IRS asks whether some of those holdings are stock in US corporations.

They think custody offshore changes the answer.

It usually does not.

That is why direct US shares matter so much for British expats, South African expats, Europeans in the Gulf, and other non-US investors who hold US-listed stocks as part of a wider international portfolio.

US-domiciled ETFs and funds

This is where the article needs to be sharper than most online explainers.

The practical risk for many expats is not a Manhattan apartment. It is a platform full of US-domiciled ETFs.

The reason is not that ETFs are inherently bad. The reason is that the legal wrapper still matters. If the holding is effectively stock in a US corporation or otherwise treated as a US situs security, the investor may have created the very exposure they thought they were avoiding by choosing a diversified product. Your own site already makes this point clearly in Hold US Shares? Read this., which notes that US-domiciled mutual funds or ETFs generally count as US situs assets for estate-tax purposes.

This is one of the biggest mistakes in cross-border investing.

People focus on market exposure when they should be checking legal exposure.

You can want exposure to US equities without necessarily wanting your estate to own US situs assets directly. Those are two different questions.

Certain debt obligations

Debt is more nuanced.

The IRS instructions say that certain debt obligations can be treated as US situs property, but they also lay out important exceptions and carve-outs. That is why fixed-income holdings need to be classified rather than guessed.

This matters because many clients hear one sweeping sentence like “US bonds are fine” or “US debt is caught” and run with it. The better answer is that debt can sit in a much more technical category, and the detail matters.

What is often outside the estate-tax net

Certain bank deposits

This is one of the most useful corrections to make because families often overestimate the risk once they first hear about US situs rules.

The IRS instructions say that certain deposits with US banks and certain similar accounts are generally treated as property located outside the United States if they are not effectively connected with a US trade or business.

That means “cash in America” is not always the same as “US estate-tax exposure”.

This distinction matters in real life. A family might panic because a spouse holds a large cash balance with a US bank, while the actual exposure may be sitting elsewhere in a brokerage account in the form of US shares or US-domiciled ETFs.

Certain qualifying debt obligations

The IRS instructions also say that certain qualifying debt obligations can be treated as located outside the US for estate-tax purposes, subject to conditions and exceptions.

This is exactly why broad, slogan-like answers are dangerous. Some US-linked debt may sit outside the estate-tax net. Some may not. You need the holding-level analysis.

Life insurance proceeds on the nonresident’s life

The IRS instructions say that proceeds of insurance on the life of a nonresident not a US citizen are treated as property outside the United States.

That does not mean every life-policy structure is automatically suitable or tax-efficient in a wider planning sense. It does mean that life insurance often appears in cross-border estate-liquidity discussions for good reason.

The biggest mistake: confusing the account with the asset

This is where most families go wrong.

They say:

- “I have a US broker”

- “I hold my investments offshore”

- “My spouse banks in the States”

- “I have a US investment account”

Those statements are not useless, but they are not the real answer either.

The account is not the same thing as the asset.

Inside one account you might have:

- US corporate shares that are generally US situs

- cash balances that may fall under the deposit exception

- qualifying debt with different treatment

- non-US holdings that are outside the issue entirely

That is why good planning on this topic always becomes a line-by-line exercise. Not because advisers like complexity, but because the IRS rules themselves are asset-specific.

This is also why executors can get into trouble. They often inherit a platform statement, not a clean classification memo. By the time they are trying to work out what needs reporting, the estate is already under pressure.

The $60,000 threshold is where this becomes real

A lot of investors hear “estate tax” and think of eight-figure families.

That is the wrong mental model here.

For a nonresident not a citizen of the United States, the executor generally must file Form 706-NA if the fair market value at death of the decedent’s US-situated assets exceeds $60,000. The IRS restated this again in January 2026.

That number is small enough that the issue can arise from:

- a modest direct US equity portfolio

- a US-domiciled ETF position

- one US property interest

- a portfolio that drifted upward over time without anyone revisiting the estate consequences

That is why this is not a “later” issue. It is a portfolio-review issue now.

Treaty relief can materially change the answer

This is the second major decision point after classification.

The IRS instructions list death tax treaties with countries including the United Kingdom, South Africa, France, Germany, the Netherlands, Switzerland, Japan, Ireland, Italy, Canada, and others.

For British expats and South African expats, this is particularly important.

Treaty relief can affect the ultimate estate-tax outcome and may improve the credit position materially. But treaty relief is not a substitute for classifying the assets correctly. It comes after the holdings review, not before it.

The correct order is:

- identify the assets

- classify the assets

- value the US situs exposure

- then review treaty relief

Too many families reverse that order. They start with “surely the treaty solves it” before they have even worked out whether they hold US situs assets in the first place.

What executors and spouses usually discover too late

This is the part most articles miss.

The technical issue is one thing. The family experience is another.

When this is left too late, what the spouse or executor often discovers is:

- nobody has prepared a clean asset map

- the account statements are not self-explanatory

- there is no note explaining which holdings are US situs and which are not

- nobody has warned them about Form 706-NA

- the estate may face delays while tax and documentation are worked through

- a “simple investment account” turns out not to be simple at all

That is why this topic belongs inside a wider estate-planning review, not just inside an investment review.

It touches:

- wills

- liquidity

- investment structure

- executor readiness

- family administration after death

Your site’s Estate Planning for Expats (2026): Wills, Guardianship, Assets makes this broader point well. Estate planning is a system, not a document, and cross-border assets are part of that system.

Five worked examples with numbers

Example 1: British expat in Dubai with $220,000 of direct US shares

This is the most common clear-cut case. Direct holdings in US corporations are generally US situs property, and the value is already well above the $60,000 threshold. The estate therefore needs a proper US estate-tax review and likely treaty analysis under the US-UK framework.

Example 2: South African family with a $900,000 Florida property

US real estate is generally US situs property. The family is outside the US in everyday life, but the asset is not outside the US estate-tax conversation. This is exactly the sort of holding that needs treaty review, liquidity planning, and clear executor instructions.

Example 3: Non-US investor with $300,000 on deposit at a US bank

This often creates unnecessary panic. Certain bank deposits are generally treated as outside the US estate-tax net if not effectively connected with a US trade or business. The existence of a US banking relationship does not automatically mean estate-tax exposure on that cash.

Example 4: UAE-based investor with $140,000 in a US-domiciled ETF

This is where the practical risk often sits. The investor thinks they own a diversified, low-cost fund. The estate-planning question is whether the legal structure means the holding is treated as a US situs asset. Your own guide on holding US shares highlights this exact issue for non-resident aliens holding US stocks and similar exposure.

Example 5: Mixed brokerage account

Suppose the account holds $80,000 in direct US shares, $120,000 in cash, and $100,000 in qualifying debt. That is not one estate-tax answer. It is three separate classification questions. The direct shares are the obvious danger. The cash may be outside scope depending on the deposit rules. The debt may need technical review. Good planning here is granular, not generic.

What to check this week if you are a British expat in the Middle East

- Pull the latest full list of holdings, not just the headline account values.

- Identify any direct US shares.

- Identify any US-domiciled ETFs or mutual funds.

- Separate bank deposits from brokerage cash and from securities.

- Ask whether the current value of likely US situs assets exceeds $60,000.

- If you are British, test the US-UK treaty angle properly.

- Make sure your spouse or executor would know that a Form 706-NA issue may exist.

- Review how this fits with your wider estate-planning structure, not just the portfolio itself.

That is the practical version of the article.

Not “learn the rules someday”.

Check what you actually own now.

Common objections

Objection

“I’m not American, so this doesn’t apply to me.”

Emotional logic

US estate tax sounds like a US-person issue.

Practical risk

For NRNC estates, the issue is US-situated assets, not everyday nationality. Direct US shares and US real estate are the classic traps.

Next step

Review the holdings, not the passport.

Objection

“My account is offshore, so the assets can’t be US situs.”

Emotional logic

Offshore custody feels like offshore treatment.

Practical risk

The IRS looks at the legal character of the asset. Stock of US corporations is generally US situs regardless of where the certificate sits.

Next step

Check the legal domicile of each holding.

Objection

“It’s only a modest portfolio.”

Emotional logic

Estate tax sounds like an ultra-wealthy problem.

Practical risk

The Form 706-NA filing threshold is only $60,000 of US-situated assets.

Next step

Measure the current value of likely US situs assets today.

Objection

“There must be a treaty, so I’m fine.”

Emotional logic

Treaty relief sounds like a complete fix.

Practical risk

Treaties can help materially, but only after the assets have been classified correctly.

Next step

Do the treaty review second, not first.

You may also like

Hold US Shares? Read this.

Estate Planning for Expats (2026): Wills, Guardianship, Assets

Hidden Tax Traps: What Those with U.S. Ties Need to Know Before Moving Abroad

A Guide for Estate Planning When Holding US Shares

Conclusion

US situs asset exposure is not mainly an American problem.

It is an ownership and classification problem.

If a non-US person owns the wrong type of US asset in the wrong way, the estate can face US filing obligations and potentially US estate-tax exposure even where the individual lived, worked, and paid tax elsewhere. The biggest practical traps are usually direct US shares, US-domiciled ETFs, and US real estate. The biggest missed opportunity is often failing to check whether treaty relief, especially for UK and South African clients, changes the result materially.

The right order is simple:

- classify the assets properly

- work out whether the $60,000 threshold is crossed

- review treaty relief

- prepare the spouse, family, and executor for what happens next

That is the difference between having a technical issue and having a manageable plan.

If you want help reviewing whether your US shares, US-domiciled funds, US property, or custody structure create estate-tax exposure, and how that fits into your broader cross-border estate plan, book a US estate planning review with Josh Clancey.

FAQ

Quick definitions

US situs asset

An asset treated as located in the United States for US estate-tax purposes.

NRNC

A nonresident not a citizen of the United States, the category relevant to Form 706-NA.

Form 706-NA

The US estate-tax return used for estates of nonresident non-citizens where the filing conditions are met.

Do direct US shares trigger estate tax for a non-US person?

They can. The IRS position is that stock of corporations organised in or under US law is generally property located in the United States.

Are US-domiciled ETFs a problem for non-US families?

They can be, because the legal structure of the holding still matters for estate-tax classification. This is one of the most common practical traps for non-US investors with US market exposure.

Are US bank deposits always exposed?

No. Certain bank deposits are generally treated as outside the United States for estate-tax purposes if they are not effectively connected with a US trade or business.

What is the filing threshold?

For an executor of a nonresident, not a citizen of the United States, Form 706-NA is generally required if the fair market value at death of the decedent’s US-situated assets exceeds $60,000.

Can a treaty improve the position?

Yes. The IRS instructions recognise death tax treaties with several countries, including the UK and South Africa.

Why does this matter so much for executors?

Because the issue is often discovered after death, when the family is already dealing with probate, grief, paperwork, and asset access. A clean holdings review in advance makes that process much easier. This is an inference based on the IRS filing framework and the practical cross-border administration issues discussed above.