How Probate Works When You Own Assets in Multiple Countries

When someone dies owning assets in more than one country, probate usually stops being one process and becomes several linked processes. One court may deal with the main estate, but other countries may still require a local grant, a resealed grant, translations, tax forms, or local executor authority before assets can be sold, transferred, or released. In England and Wales, foreign assets may also need to be reported on form IHT417 where relevant.

Entity list

HMRC, IHT417, Form IHT400, Probate Registry, Colonial Probates Act, Non-Contentious Probate Rules 1987, DIFC Courts, Dubai Courts, cross-border estate administration, executor pack

People also ask

What happens if someone dies owning assets in more than one country?

Is one grant of probate enough for worldwide assets?

What is resealing a foreign grant of probate?

When do you need local probate in another country?

Can a UK grant of probate be used overseas?

How do UAE assets fit into a cross-border estate?

What slows down international probate the most?

How can expats make multi-country probate easier for their family?

At a glance

- Multi-country probate is usually not one probate case. It is one death triggering several legal and administrative processes across different countries. This is an inference from how HMRC, the UK resealing process, and DIFC probate execution operate in practice.

- A grant from one country is often not automatically enough to deal with assets in another. Some jurisdictions require a fresh local grant. Others may recognise or reseal a foreign grant.

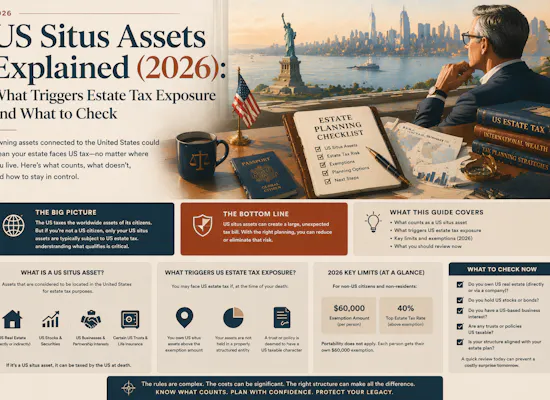

- In England and Wales, if the deceased had a permanent home in the UK and owned foreign assets, HMRC says form IHT417 is used with IHT400 for foreign assets.

- In England and Wales, resealing is available for grants from certain jurisdictions covered by the Colonial Probates Acts and the procedure is governed by rule 39 of the Non-Contentious Probate Rules 1987.

- For UAE-linked estates using the DIFC Wills system, DIFC Courts state that probate orders still require execution at the Dubai Courts as a standard formality.

- The biggest delays usually come from missing documents, conflicting wills, poor asset maps, local bank freezes, translation requirements, tax filings, and families discovering too late that a home-country will did not solve local administration. This is an inference supported by HMRC, DIFC, and your own estate-planning content.

Opening

When people think about probate, they usually imagine one executor, one court, and one estate process.

That is not how it feels when assets sit in London, Dubai, South Africa, Singapore, and the US at the same time.

Then probate becomes an operations problem.

One death can trigger:

- a UK probate application

- a local court process elsewhere

- bank freezes in one country

- registrar requirements in another

- translations and legalisations

- tax forms that have to be filed before authority is released

- and a spouse or executor trying to work out which document works where

That is the real issue.

If you own assets in multiple countries, probate usually stops being a single legal event and becomes a chain of linked processes that have to be coordinated in the right order. HMRC’s foreign-assets form, the UK resealing framework, and the DIFC probate process all point in the same direction: cross-border estates are administrative systems, not just documents.

That is why the families who cope best are rarely the ones with the most paperwork.

They are the ones with the clearest asset map, document map, and executor instructions.

The key principle: one death, multiple authorities

The first thing to understand is that probate authority is territorial.

A grant from one country proves authority in that system. It does not automatically unlock every asset worldwide.

That means three broad outcomes are common:

One country issues the main grant, other countries require local steps

This is the most common pattern. You may have a main probate process in the country of domicile, habitual residence, or the country holding the core estate, but banks, registrars, land departments, and courts in other countries may still require their own authority before they will release or transfer assets.

A foreign grant can sometimes be resealed

In England and Wales, a foreign grant from certain jurisdictions can be resealed rather than forcing a full fresh probate application. The Gazette explains that this applies where the Colonial Probates Acts apply, and that rule 39 of the Non-Contentious Probate Rules 1987 governs the procedure.

Some countries insist on their own local process

This is often the case where the asset is locally registered, the court wants local executor authority, or the legal system does not simply recognise the foreign grant. UAE-linked estates are a good example of why local execution still matters. DIFC states that its probate orders require execution at the Dubai Courts as a standard formality.

That is why “we already got probate in country A” is often only the beginning.

What probate is really trying to do

Strip away the jargon and probate is trying to answer four practical questions:

- Who has legal authority to act?

- What assets exist, and in which countries?

- What taxes, declarations, or court steps are required before transfer?

- Who can actually access cash quickly enough to keep life moving?

Your own estate-planning article gets this right. Cross-border estate plans fail at the seams between countries, documents, nominations, and liquidity. The goal is not just to have a will. It is to make the estate work operationally after death.

That is the frame families should use.

Not “Do we have a will?”

But “Would the right person be able to act in the first week, first month, and first six months?”

Why one grant is often not enough

There are several reasons one grant may not solve everything.

Asset holders answer to local law and local process

A bank in Dubai, a registrar in England, a land office in Spain, and a custodian in the US do not all answer to the same probate document or the same court.

Local forms and tax filings may be needed first

In the UK, HMRC says that if the deceased had a permanent home in the UK and had assets outside the UK, form IHT417 is used with IHT400 for those foreign assets. That shows how even the UK probate and tax side already expects cross-border estates to need extra reporting.

Some jurisdictions require recognition or execution steps

Even where you have a well-structured will system, you may still need a second procedural step. DIFC’s own FAQ says probate orders require execution at the Dubai Courts as a standard formality.

Different assets behave differently

A pension death benefit, a nominee account, a jointly held bank balance, a directly registered property, and a private company shareholding may each require a different process. Probate is not one uniform switch that unlocks everything at once.

Resealing: where it can help, and what it actually means

Resealing is one of the most useful concepts in international probate because it can reduce duplication.

The Gazette explains that resealing means a foreign grant is re-issued so it becomes effective to administer the estate in England and Wales. It also notes that this can avoid the expense and inconvenience of taking out a fresh grant where the relevant Colonial Probates Acts apply.

That makes resealing attractive because it can:

- save time compared with a completely new application

- preserve continuity of the personal representatives already appointed

- make it easier to deal with UK assets after an overseas grant has been obtained

But it is not universal.

The same Gazette article notes that resealing in England and Wales applies only to grants from the jurisdictions covered by the relevant legislation, broadly many old Commonwealth jurisdictions, and points to the Colonial Probate Act Application Order 1965.

So the correct question is not “Can foreign probate be recognised?”

It is “Can this particular foreign grant be resealed in this particular jurisdiction?”

That is a narrower question and a much more useful one.

How UAE-linked probate fits into a multi-country estate

For expat families in the Middle East, this is often where the administration gets real.

A UK will may work well for UK assets. It does not automatically mean UAE banks, property, or local institutions will move quickly. Your own UAE will article makes this point bluntly: a home-country will alone often does not prevent UAE account freezes and local succession delays.

Where a DIFC will is in place, DIFC says its probate orders still require execution at the Dubai Courts as a standard formality, though it also says the new law has clarified smoother enforcement.

The practical lesson is straightforward:

- UK document for UK assets

- UAE-executable route for UAE friction points

- coordination between the two so they do not clash

That is why cross-border estates often need coordinated wills, not necessarily one global document trying to do everything.

The real reasons international probate gets delayed

Families often assume the delay is mainly legal complexity.

Sometimes it is.

More often, it is missing administration.

No clean asset map

Executors cannot move quickly if they do not know what exists, where it is held, how it is owned, and which documents control it. Your own estate-planning content repeatedly emphasises the need for an asset map and executor pack.

Conflicting wills or uncoordinated documents

A UK will, a UAE will, old beneficiary forms, and informal instructions can easily create uncertainty if they were never coordinated.

The family discovers local process too late

This is common with UAE bank balances, property, and local succession steps. By the time the spouse learns that the UK grant is not enough, the estate is already in reactive mode.

Documents need translation, certification, or legalisation

This is a classic cross-border slowdown. It is not dramatic, but it is time-consuming and expensive.

Tax and reporting issues are incomplete

HMRC’s IHT417 is one example. HMRC’s February 2026 Trusts and Estates Newsletter also warned about practical bereavement correspondence issues and reminded estates not to miss cryptoassets on IHT returns.

No one has immediate access to liquidity

This is often the real family crisis. The estate may be wealthy, but if the spouse cannot access working cash in the first 30 to 90 days, probate becomes an emotional and operational problem, not just a legal one.

Five worked examples with numbers

Example 1: UK plus UAE estate

- UK assets: £650,000

- UAE cash and investments: AED 900,000

- No UAE will

- UK will in place

This is a common expat setup. The UK will may support the UK grant, but UAE asset access can still be slow if there is no UAE-executable route. The family may face parallel processes rather than one clean handover. Your UAE will article explicitly warns that a home-country will alone often does not prevent UAE freezes and delays.

Example 2: South African grant, English assets

- Main estate in South Africa

- London share portfolio worth £280,000

- South African grant already obtained

This may be a resealing case rather than a full fresh English probate case, depending on the jurisdictional eligibility and the documents available. The Gazette explains that resealing can be used for grants from relevant jurisdictions covered by the Colonial Probates Acts.

Example 3: UK resident with foreign assets

- UK home and bank accounts

- French property

- Singapore brokerage account

- UK resident at death

In the UK, the estate may need foreign assets reported to HMRC on IHT417 with IHT400. That does not solve the French or Singapore administration by itself, but it shows that even the UK side expects a broader reporting exercise.

Example 4: DIFC will plus UK assets

- DIFC-registered will for Dubai assets

- UK ISA and pension

- Joint UAE account

- Child living in Dubai

This is likely a coordinated multi-channel estate rather than one probate lane. DIFC probate may help with UAE execution, but UK assets still need UK processes, and pensions may run outside the will through nominations. DIFC also states that probate orders require execution at the Dubai Courts as a standard formality.

Example 5: No asset map, three jurisdictions

- UK pension and bank accounts

- UAE current accounts

- US brokerage account

- Surviving spouse does not know providers or account numbers

This is where estates lose months unnecessarily. The legal difficulty is real, but the first failure is administrative. Without an asset map and executor pack, the family starts blind. Your own estate-planning content flags this repeatedly.

What executors actually need

The strongest multi-country estates usually have a simple pack that answers practical questions quickly.

That pack should usually include:

- a full asset list by country

- account numbers and provider names

- which will applies where

- who the executors are in each jurisdiction

- where original documents are held

- key advisers by country

- beneficiary nominations on pensions and insurance

- emergency liquidity instructions

- passport, visa, property, company, and trust details where relevant

This is not overkill.

It is what turns a cross-border estate from chaos into something manageable.

What to do now if your estate spans countries

- Build a country-by-country asset map

List what is owned, where it is located, how it is held, and whether it passes by will, nomination, survivorship, or company structure. - Check whether one grant will be enough anywhere

Assume the answer is no until confirmed. Then test where resealing or local probate may apply. - Coordinate wills rather than stacking random documents

This is especially important for UK and UAE combinations. - Plan for liquidity, not just inheritance

Ask how the family gets cash in the first 30 to 90 days. - Prepare the executor pack before it is needed

This is one of the highest-return estate-planning tasks an expat family can do.

Common objections

Objection

“We already have a will, so probate should be straightforward.”

Emotional logic

A signed will feels like the main thing that matters.

Practical risk

A will helps with intent, but not every country will accept the same grant or process. Local recognition, resealing, tax forms, and execution steps may still be needed.

Next step

Check not just whether you have a will, but whether each jurisdiction has an executable route.

Objection

“My spouse will be able to sort it out.”

Emotional logic

Families often assume the surviving spouse can just step in.

Practical risk

Without authority, account details, and local documents, the spouse may spend months just identifying what exists and who will release it.

Next step

Prepare the asset map and executor pack now.

Objection

“Most of my wealth is digital or investment-based, so it should be easier.”

Emotional logic

Online access feels simpler than bricks and mortar.

Practical risk

Custodians and brokers still follow legal authority rules. HMRC also reminded estates in 2026 not to miss cryptoassets on IHT returns.

Next step

Document provider access, ownership, and death-administration process for each holding.

Objection

“I only need to think about tax, not probate.”

Emotional logic

Tax often feels like the more technical issue.

Practical risk

Families do not experience estates as tax problems first. They experience them as access, authority, and delay problems first.

Next step

Treat tax and probate as linked, but separate, planning tasks.

You may also like

Estate Planning for Expats (2026): Wills, Guardianship, Assets

Do Non-Muslim Expats Need a Will in the UAE? (2026 Guide)

Cross-Border Estate Planning Checklist for Expats 2026

US Estate Tax for Expats in 2026: Basics That Still Matter

Conclusion

Multi-country probate is rarely about one dramatic legal problem.

It is usually about several ordinary problems happening at once:

- the wrong document in the wrong country

- the right document, but no local authority

- the grant that works in one place but not another

- the bank account that freezes before the family has cash

- the executor who has the title but not the map

That is why the best cross-border estate plans are operational.

They do not just say who gets what.

They show who can act, where they can act, and how quickly the family can get through the first 90 days.

If you own assets in more than one country, the planning standard should be simple: each country should have a clear path from death certificate to legal authority to asset access. Anything less is leaving your family to solve an operations problem while grieving.

If you want help pressure-testing your current wills, asset map, executor pack, and cross-border probate weak points, book a cross-border estate planning call with Josh Clancey.

FAQ

Quick definitions

Grant of probate

A court document confirming authority to deal with an estate under the relevant legal system.

Resealing

In England and Wales, the process by which certain foreign grants are re-issued so they become effective for administering assets there.

IHT417

HMRC’s form for foreign assets, used with IHT400 where the deceased had a permanent home in the UK and assets outside the UK.

Executor pack

A practical set of documents and instructions showing what exists, where it is held, and how the estate is meant to be administered. This is a planning term rather than a statutory one, but it is central to workable cross-border estate administration.

Is one grant of probate enough for worldwide assets?

Usually no. One grant may deal with the main estate, but other countries may require local recognition, resealing, or a fresh grant before assets can be released.

What is resealing a foreign grant of probate?

It is the process of re-issuing an eligible foreign grant so it becomes effective in England and Wales. The Gazette explains that this can avoid taking out a fresh grant where the Colonial Probates Acts apply.

Do UK probate forms cover foreign assets too?

Yes, where relevant. HMRC says IHT417 is used with IHT400 if the deceased had a permanent home in the UK and foreign assets.

Can a UK will solve UAE asset administration on its own?

Often not. Your UAE will article notes that a home-country will alone often does not prevent UAE account freezes and local succession delays. DIFC also says its probate orders require Dubai Court execution as a standard formality.

What slows down international probate the most?

Missing asset information, conflicting documents, lack of local authority, translation and certification steps, and poor family liquidity planning are the most common blockers. This is an inference supported by HMRC, DIFC, and your own estate-planning material.

What is the best way to make multi-country probate easier?

Create a country-by-country asset map, coordinate wills, confirm where local probate or resealing may be needed, and prepare an executor pack before it is needed.