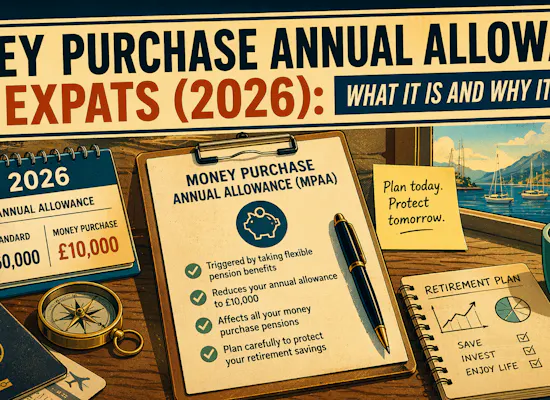

Money Purchase Annual Allowance for Expats: What It Is and Why It Matters

The Money Purchase Annual Allowance is a reduced annual allowance that usually applies after you first flexibly access taxable money from a defined contribution pension. In 2026 to 2027, the MPAA is £10,000. It matters because once triggered, future money purchase pension contributions above that level can create an annual allowance tax charge.

People also ask

- What is the Money Purchase Annual Allowance?

- What triggers the MPAA in 2026?

- Does taking 25% tax-free cash trigger the MPAA?

- Does the MPAA affect defined benefit pensions?

- Can British expats still contribute to a pension after triggering the MPAA?

- Why does the MPAA matter if you live in the UAE?

At a glance

- The MPAA is £10,000 for the 2026 to 2027 tax year.

- It usually applies once you flexibly access taxable money from a defined contribution pension.

- Taking only the 25% tax-free lump sum and leaving the rest invested usually does not trigger it.

- Taking benefits from a defined benefit pension does not usually trigger the MPAA.

- Once triggered, the MPAA applies in the tax year of the trigger event and future tax years.

- For expats, the MPAA matters because a pension access decision made while abroad can reduce how much you can later contribute with tax relief if you return to the UK, resume UK earnings, or keep building pension savings.

Most expats do not worry about the Money Purchase Annual Allowance until after they have triggered it.

That is the problem.

The MPAA is one of those rules that looks small, technical, and easy to ignore right up until the moment it blocks a bigger retirement plan. A British expat in Dubai might take money from a defined contribution pension because it feels tidy, tax-efficient, or simply convenient. Years later, they are back in the UK, earning well again, or making larger pension contributions through a business, and suddenly discover they permanently shrank one of their most useful pension tax allowances.

That is why this topic matters.

The MPAA is not mainly about whether you can take money from a pension. It is about whether the way you take that money quietly damages your future contribution flexibility.

What is the Money Purchase Annual Allowance?

The MPAA is a reduced annual allowance that usually applies after you first flexibly access a money purchase pension in certain ways. HMRC’s pension rates page confirms the MPAA is £10,000 for 2026 to 2027, while the standard annual allowance is £60,000.

That difference is the whole issue.

Before the MPAA is triggered, many people can potentially contribute up to the normal annual allowance, subject to earnings, tapering, and other rules. After it is triggered, the allowance for money purchase pension inputs is much lower. MoneyHelper explains that once the MPAA applies, contributions from you and your employer to defined contribution pensions generally need to stay within £10,000 a year to avoid extra tax charges.

So this is not a minor technical footnote. It is a rule that can cut future contribution capacity sharply.

Why it exists

The MPAA was introduced to stop people taking taxable money from a pension and then cycling it back in to get more tax relief. HMRC’s legislation pages frame it around people who have flexibly accessed money purchase benefits.

That anti-recycling purpose is why the rule is triggered by some forms of flexible access and not others.

In practice, this means the government is not trying to stop ordinary retirement decisions altogether. It is trying to stop people from taking taxable pension money and then rebuilding pension contributions with fresh tax relief in a way the rules see as abusive.

What triggers the MPAA?

This is the section most people should read twice.

MoneyHelper says the MPAA is normally triggered if you do any of the following from a defined contribution pension:

- start taking your pension as a series of lump sums

- take a regular income using pension drawdown or from an investment-linked or flexible annuity where the income is not guaranteed

- take your entire pension in one go, unless it qualifies under the small pots rules

- exceed the cap on old capped drawdown arrangements started before April 2015.

HMRC’s manual says a trigger event determines when someone first flexibly accesses a money purchase arrangement, and once that happens the MPAA applies for that tax year and later years.

The practical takeaway is simple:

taking taxable flexible income is the danger zone.

What does not usually trigger the MPAA?

This matters just as much.

MoneyHelper says the MPAA is usually not triggered if you:

- take up to 25% as tax-free cash and leave the rest invested

- use the remaining pot to buy a guaranteed lifetime annuity

- take money from a defined benefit pension.

This is one of the most useful distinctions for expats.

A lot of people assume “any pension access triggers MPAA.” That is wrong. The problem is not pension access in general. The problem is flexible taxable access to money purchase pensions.

So if someone takes only the pension commencement lump sum and does not draw taxable income, the MPAA usually does not bite at that stage.

Why this matters specifically for expats

At first glance, the MPAA can seem like a UK resident problem.

It is not.

It matters for expats because pension decisions made while living abroad can affect what you can do later if any of the following happen:

- you return to the UK

- you start earning UK-taxable income again

- you keep contributing to a UK pension while abroad

- your employer continues pension contributions

- you sell a business and want to accelerate pension funding

- you move from “drawing a bit now” to “serious retirement planning later”

That is why the rule catches expats out. A temporary, tactical decision abroad can create a long-term contribution constraint.

For a British expat in the Middle East, this is especially relevant. Life abroad often feels administratively separate from future UK planning. In reality, the pension tax framework follows you more than many people expect.

MPAA and defined benefit pensions

This is another area people misunderstand.

MoneyHelper says the MPAA does not affect you if you only have a defined benefit pension. But if you have both defined contribution and defined benefit pensions, you can also have an alternative annual allowance for the non-money-purchase side.

HMRC’s rates page shows that for 2026 to 2027 the alternative annual allowance is generally £50,000, being the annual allowance less the MPAA where the rules apply.

This means the MPAA does not simply destroy all pension planning after a trigger event. But it does reduce flexibility on the money purchase side and can make future planning much clumsier.

Five worked examples with numbers

UAE expat takes flexible income at 56

David lives in Dubai and draws £15,000 of taxable income from a UK drawdown plan at 56. That usually triggers the MPAA. Five years later he returns to the UK and wants to contribute £30,000 a year into a SIPP. He now has a £10,000 money purchase limit, not the usual £60,000.

Qatar-based expat takes only tax-free cash

Emma takes only her 25% tax-free lump sum from a UK defined contribution pension and leaves the rest untouched. On MoneyHelper’s guidance, that usually does not trigger the MPAA.

Bahrain resident empties a pot

Simon cashes out a pension worth £90,000 in one go. Unless this fits the small pots rules, that will normally trigger the MPAA because he has taken taxable money flexibly.

Oman-based expat with DB and DC schemes

Rachel flexibly accesses a DC pot and later continues accruing benefits in a DB arrangement. The MPAA restricts her money purchase inputs, but HMRC’s rules still allow an alternative annual allowance for the other pension inputs.

Return-to-UK business owner

Mark lives in Abu Dhabi, triggers the MPAA at 55, then returns to the UK at 59 and wants his company to pay £40,000 a year into his pension. He discovers too late that the money purchase side is capped at £10,000 before tax-charge issues arise.

What people often overlook

The biggest blind spot is that the MPAA is usually permanent for future tax years once triggered. HMRC’s manual says it applies in the tax year of the trigger event and subsequent tax years.

The second blind spot is that this is not mainly about retirees. It is often more damaging for people who are not finished saving yet.

The third is that providers have reporting obligations. MoneyHelper says your provider must send a flexible access statement within 31 days, or 91 days if it involves an overseas pension, and you may then need to tell other active DC schemes within 91 days.

That administrative point matters because the MPAA is not just a concept. It creates reporting consequences too.

Common objections

Objection

“I’m living abroad, so this probably doesn’t matter.”

Emotional logic

Life abroad feels separate from future UK pension planning.

Practical risk

A trigger event abroad can still cut future contribution flexibility if you later return or keep funding pensions.

Next step

Treat every pension access decision abroad as part of your long-term UK retirement plan.

Objection

“I’m only taking a bit, so it won’t matter.”

Emotional logic

A small withdrawal feels harmless.

Practical risk

Even a modest taxable flexible withdrawal can trigger the MPAA.

Next step

Check whether the access method, not just the amount, is the trigger.

Objection

“I’ve got a final salary pension too, so I’m fine.”

Emotional logic

Another pension arrangement feels like a safety net.

Practical risk

The MPAA can still restrict the DC side even if DB accrual continues.

Next step

Model both sides together before accessing any taxable DC money.

People also ask

What is the Money Purchase Annual Allowance?

It is a reduced annual allowance that usually applies after you first flexibly access taxable money from a defined contribution pension. In 2026 to 2027, it is £10,000.

Does taking 25% tax-free cash trigger the MPAA?

Usually no, if you only take the tax-free lump sum and do not start taxable flexible withdrawals.

Does the MPAA apply to defined benefit pensions?

Not by itself. If you only have a defined benefit pension, the MPAA does not usually affect you.

Why does the MPAA matter for UAE expats?

Because a pension access decision made in the UAE can still limit how much you can contribute with tax relief later if you return to the UK or continue pension funding.

Can I still contribute to a pension after triggering the MPAA?

Yes, but the money purchase side is generally limited to £10,000 a year before extra tax-charge issues arise.

Does carry forward solve the MPAA?

Not in the normal way for the money purchase side once the MPAA has been triggered. HMRC’s framework instead applies the MPAA and, where relevant, the alternative annual allowance.

You may also like

UK Expat Retirement Planning Timeline (2026): What to Do in Your 30s, 40s, 50s, 60s

SIPP vs QROPS vs QNUPS: What Each Does for Expats

UK Pension Transfers for Expats (2026): SIPP, QROPS, Consolidation

Should I Consolidate UK Workplace Pensions in 2026?

Should You Transfer Your UK Pension Abroad? Decision Framework (2026)

Conclusion

The Money Purchase Annual Allowance is one of those rules that seems small until it materially shrinks your options.

For expats, that is why it matters.

The risk is not simply that you take money from a pension. The risk is that you take it in the wrong way, trigger the MPAA, and only later realise you have damaged your future contribution flexibility just when your retirement planning becomes more serious.

That is why the best question is not:

“Can I access my pension?”

It is:

“Will the way I access it quietly reduce what I can still do later?”

If you want help reviewing whether your pension access plans could trigger the MPAA, and how that fits into your wider cross-border retirement plan, book a pension planning call with Josh Clancey.

FAQ

Quick definitions

MPAA

The Money Purchase Annual Allowance, a reduced annual allowance that usually applies after taxable flexible access to a defined contribution pension.

Trigger event

The event that first causes the MPAA rules to apply after flexible access to a money purchase arrangement.

Alternative annual allowance

The allowance that can still apply for other pension inputs, such as defined benefit accrual, where MPAA rules are in play.

What is the MPAA in 2026 to 2027?

It is £10,000.

What normally triggers the MPAA?

Usually taking taxable money flexibly from a defined contribution pension, such as flexible drawdown income or UFPLS-style lump sums.

Is taking tax-free cash enough to trigger it?

Usually no, if you only take the tax-free element and do not start taxable flexible withdrawals.

Does it matter if I live abroad?

Yes, because a trigger abroad can still affect future UK pension contribution planning.

Do providers have to tell me if I trigger it?

Yes. MoneyHelper says providers must usually send a flexible access statement within 31 days, or 91 days for an overseas pension.