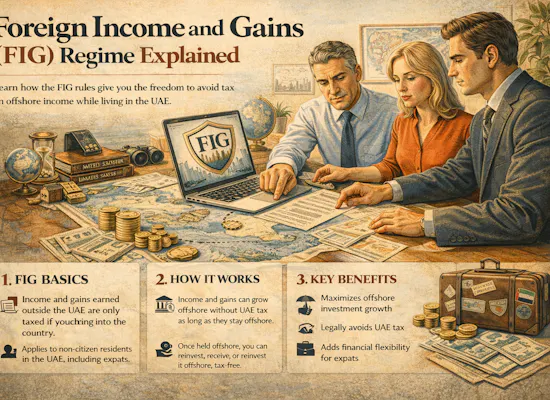

Foreign Income and Gains (FIG) regime explained

The UK Foreign Income and Gains regime lets qualifying new UK residents claim relief on eligible foreign income and gains for up to 4 tax years, provided they were non-UK resident for at least 10 consecutive tax years before becoming UK resident. It replaced the remittance basis from 6 April 2025 and must be claimed through Self Assessment.

People also ask

- What is the Foreign Income and Gains regime in the UK?

- Who qualifies for the 4-year FIG regime?

- Does the FIG regime replace the remittance basis?

- Can British expats in Dubai use the FIG regime when returning to the UK?

- Does the FIG regime cover foreign salary and bonuses?

- Do you lose your personal allowance if you claim FIG relief?

- What happens to offshore income and gains built up before 6 April 2025?

- Is the FIG regime automatic or do you have to claim it?

At a glance

- The FIG regime replaced the remittance basis from 6 April 2025.

- It is based on residence, not domicile. The key test is whether you are a qualifying new resident.

- You generally need 10 consecutive tax years of non-UK residence before the relevant year of UK residence to qualify.

- Relief can apply for up to 4 tax years from the start of UK residence, but unused years do not roll forward just because you chose not to claim.

- The regime is not automatic. You claim it through Self Assessment, using SA109 and the relevant supplementary pages.

- You do not need to claim on all foreign sources. Relief is claimed source by source, and there is no cap on the amount of eligible relief.

- Foreign dividends, overseas property business profits and foreign capital gains can be within scope, but foreign employment income is not relieved under FIG itself.

- If you claim FIG relief, you lose your personal allowance, CGT annual exempt amount and certain other allowances and tax reductions.

- Pre-6 April 2025 offshore income and gains are a separate issue. The Temporary Repatriation Facility may help in some cases, at 12% in 2025-26 and 2026-27, and 15% in 2027-28.

- For most expats, the real question is not “Can I claim FIG?” It is “What should I do before UK residence starts, during the 4-year window, and after it ends?” That is where the planning value sits.

The real issue is not the rule. It is the timing

Most articles on the Foreign Income and Gains regime make the same mistake. They explain the rule, define the acronym, mention that the remittance basis has gone, and stop there.

That is not enough.

For a British expat in the Middle East, the FIG regime is not interesting because it exists. It matters because it changes the order in which you should make decisions before returning to the UK. A disposal in March instead of May, a bonus paid in the wrong period, mixed offshore funds left unpicked apart, or an assumption that all “foreign” receipts are covered can change the outcome materially.

The new regime was introduced from 6 April 2025 to replace the remittance basis, and it allows qualifying new residents to claim relief on eligible foreign income and gains arising during their first 4 years of UK residence. That is the rule. But the planning question is sharper than that: what should you trigger before UK residence begins, what should you leave until after arrival, and what should you not assume FIG will solve?

If you are living in Dubai, Abu Dhabi, Doha, Riyadh, Muscat or Manama and a UK return is even a medium-term possibility, FIG is not a point for later. It belongs in the pre-return checklist now.

What the FIG regime actually does

At its core, the FIG regime lets a qualifying new resident claim UK tax relief on eligible foreign income and gains arising during the first 4 years of UK residence. If a valid claim is made, UK tax is not charged on those claimed qualifying amounts, and HMRC says those relieved FIG amounts can be brought to the UK without an additional tax charge.

That last point matters because it is one of the clearest differences from the old mental model many expats still carry around. Under the remittance basis, the question often became “have I brought the money to the UK?” Under the new FIG regime, for qualifying post-6 April 2025 foreign income and gains, the focus is first on eligibility and claim mechanics. HMRC’s technical note is explicit that qualifying individuals will be able to remit those relieved funds to the UK free from additional charges.

The claim is not one blanket election that magically covers everything offshore. HMRC’s 2026 FIG helpsheet says you must complete the residence and FIG pages of the tax return and claim the relief on the relevant supplementary pages, depending on the nature of the income or gains. It also states that you do not need to claim on all sources, but you must claim for each amount of foreign income, from each source, that you want relieved.

That means the regime can be flexible, but it also means sloppy records are dangerous. If you have offshore accounts, investments, private company dividends, property income and realised gains all moving around at the same time, the tax return needs to be able to support what is being claimed and what is not. FIG is simpler than the old remittance basis in some respects, but it is not a substitute for proper classification.

Who qualifies, and where people get caught out

HMRC’s manual says an individual can be a qualifying new resident if they are UK resident in the relevant tax year and have not been UK resident for at least 10 consecutive tax years immediately before that year, subject to a couple of additional conditions. The rule is not limited to first-time arrivers. A returning Brit who left the UK for an extended period may still qualify.

This is one reason the regime is highly relevant for British expats in the Middle East. Many will have been abroad long enough to meet the 10-year condition. But many will not. Some have had a short return stint. Some were UK resident unexpectedly because of day counts, work ties or family ties. Some assume that “I lived in Dubai for years” is the same thing as “I was non-UK resident for 10 full tax years”. It is not.

The transition rules matter too. HMRC says that if your first 4 years of UK tax residence began before 6 April 2025, you may still be able to use the FIG regime from 2025-26 to the end of that original 4-year period. In other words, some people who became UK resident in 2022-23, 2023-24 or 2024-25 after a sufficient non-residence period can still access the regime for the remaining eligible years.

There is another trap. If you leave the UK temporarily during the 4-year period and become non-UK resident, HMRC says you cannot claim the regime for those years, although you may still claim for remaining qualifying years when you return. So the “4-year regime” is not always 4 clean, continuous years in practice.

For ranking and for real planning, this is the key takeaway: eligibility is factual, not assumed.

What FIG covers, and what it does not

The FIG regime can apply to a wide range of qualifying foreign income and gains. HMRC’s helpsheet lists examples including profits of a trade carried on wholly outside the UK, a UK resident partner’s share of overseas trading profits, profits of an overseas property business, and dividends from non-UK resident companies. Foreign gains can also be relieved where they are qualifying foreign gains and properly claimed.

That makes the regime potentially valuable for expats with investment income, offshore portfolios, overseas rental property, or non-UK shareholdings. For some returnees, particularly those with sizeable passive income or a plan to realise gains after coming back, the regime can create a genuinely useful planning window.

But this is where many people go wrong: not everything foreign is FIG.

HMRC is explicit that relevant foreign earnings and foreign specific employment income are not qualifying foreign income for the purposes of a FIG foreign income claim. In plain English, foreign salary, bonus and some employment-linked receipts do not simply become tax-free because they are overseas in origin. Those need separate analysis, and in some cases the relevant relief is Overseas Workday Relief, not FIG itself.

There is also disqualified income. HMRC says certain settlements income, certain transferred income streams, performance income, and some pension income are outside the relief and taxed when they arise. That is another reason broad-brush planning can backfire.

The practical point is simple: the words “foreign income” are not enough. You need to know what category the receipt falls into.

Overseas Workday Relief sits next to FIG, not inside it

For high earners and internationally mobile professionals, the biggest mistake is often assuming the whole return-to-UK question can be solved by FIG alone.

OWR continues from 6 April 2025 in changed form. GOV.UK says the post-2025 rules are now tied into the new residence-based framework, and the relief is subject to an annual financial limit for each qualifying year of the lower of 30% of qualifying employment income or £300,000.

That matters for bankers, senior executives, lawyers, consultants and business owners with trailing compensation, deferred bonuses, carried elements, global mobility arrangements or overseas work patterns after returning to the UK. These cases are rarely “just FIG”. They are usually a combined exercise involving residence, split-year treatment, employment source analysis and OWR claim discipline.

For some readers, this will be the central planning point in the whole article: FIG is excellent for the right kind of income. It is not a universal shield for return-year remuneration.

The hidden cost of claiming FIG

A strong article on FIG has to cover the downside properly, because this is where many generic explainers are weak.

HMRC states that if you claim relief under the FIG regime you lose a range of allowances and tax reductions, including the personal allowance, the CGT annual exempt amount, blind person’s allowance, and tax reductions or transferable allowances for married couples and civil partners. HMRC also says these are lost even if you only claim on foreign income, only claim on foreign gains, or only make an OWR election.

That does not mean claiming FIG is a bad idea. Far from it. In many cases the relief can still be highly valuable. But it does mean the claim should be assessed, not assumed.

HMRC also says any foreign income relief is disregarded for the purpose of calculating adjusted net income, which is relevant for matters including tax-free childcare and the High Income Child Benefit Charge. So even relieved foreign income can still have knock-on effects elsewhere in the tax system.

There is also a pensions point that gets overlooked. HMRC says a foreign income claim may restrict the amount of pension tax relief available above the basic amount in some cases. That is another reason your tax return, pension contributions and return-year planning should not be treated in separate silos.

What usually gets missed before the move back to the UK

In practice, the best FIG planning often happens before the person is UK resident again.

The first thing that gets missed is the residence timeline itself. If you do not know when UK residence starts, you cannot sensibly separate what happened before the UK came back into scope from what happened afterwards. That is why the Statutory Residence Test and split-year treatment still sit at the centre of the analysis.

The second thing is account hygiene. Many expats have capital, old income, pre-2025 gains, dividends, salaries and new investment proceeds mixed together offshore. Under the old remittance basis that caused one set of tracing issues. Under the new world, older pre-6 April 2025 funds are still highly relevant, because FIG does not rewrite history.

The third thing is disposal timing. A foreign share sale or property disposal just before UK residence starts can be a very different tax story from the same disposal a month after arrival. The answer is not always “do it before you come back”, but the fact pattern absolutely matters.

The fourth thing is behavioural. Many returnees think “I’ll sort the tax once I’m home and settled”. By then, the best timing decisions may already be gone.

Five worked examples with numbers

Example 1: Dubai investor returning with offshore dividends

Rachel has lived in Dubai for 12 consecutive tax years and becomes UK resident again in 2026-27. In that year she receives £80,000 of dividends from a non-UK company and £25,000 of overseas property profits.

Those are exactly the sort of categories HMRC lists as potentially qualifying foreign income. If she is a qualifying new resident and makes the claim properly, the income may be relieved under FIG. But she still loses the personal allowance and CGT annual exempt amount for that year if she claims.

Planning point: this is not just “can I claim?” It is “is the value of the relief worth more than the allowances I give up?”

Example 2: Qatar executive with a trailing bonus

Tom returns to the UK after 11 non-resident tax years. In year 1 of residence he receives a £220,000 bonus connected to overseas employment duties and also £30,000 of non-UK dividends.

The dividends may be in FIG territory if properly claimed. The bonus is not automatically FIG income. HMRC says foreign employment income is not qualifying foreign income for the claim. The employment element needs separate OWR and timing analysis.

Planning point: two foreign receipts in the same bank account can have completely different UK tax treatment.

Example 3: UAE returnee with old remittance-basis funds

James used the remittance basis before 6 April 2025 and has £600,000 of pre-2025 foreign income and gains sitting offshore. He returns to the UK after more than 10 non-resident tax years and assumes FIG lets him bring everything back tax-free.

It does not. HMRC says foreign income and gains that arose before 6 April 2025 while he was UK resident and using the remittance basis cannot be relieved under the FIG regime. However, the Temporary Repatriation Facility may allow designation at 12% in 2025-26 and 2026-27, and 15% in 2027-28, with future remittance of designated capital without further tax charges.

Planning point: old offshore money and new FIG money are not the same pot.

Example 4: Family returning with childcare assumptions

A couple returns from Abu Dhabi. One spouse claims FIG relief on £90,000 of foreign investment income and assumes that income disappears for all UK threshold purposes.

HMRC says foreign income relief under FIG is disregarded for ANI purposes used in rules such as tax-free childcare and the High Income Child Benefit Charge.

Planning point: relieved income can still matter for family tax outcomes.

Example 5: High earner with OWR cap pressure

A senior professional returns after 10 years abroad and has £900,000 of qualifying employment income in a year where overseas duties are still material. OWR may be available, but HMRC says the annual financial limit is the lower of 30% of qualifying employment income or £300,000. Thirty per cent of £900,000 is £270,000, so on these simplified numbers the cap would be £270,000, not the full amount of overseas-related income.

Planning point: on larger packages, the cap matters quickly.

What people misunderstand most often

The first misunderstanding is that FIG is a rebranded remittance basis. It is not. It sits in a different policy framework, is based on residence rather than domicile, and has a different set of claim mechanics and consequences.

The second is that there is one decision called “use FIG”. In reality there are several separate decisions: do you qualify, which sources should be claimed, which should not, what happens to employment income, what old pre-2025 funds exist, and what should be done before residence starts.

The third is that the move itself is the main event. It usually is not. The main event is the sequencing around the move.

Common mistakes

- Assuming years abroad automatically equal 10 qualifying non-resident tax years.

Residence status needs checking, not storytelling. - Treating all foreign receipts as FIG-eligible.

Employment income is the classic mistake. - Ignoring what is lost when a claim is made.

The personal allowance and CGT annual exempt amount are not minor details. - Not separating pre-6 April 2025 funds from post-2025 income and gains.

This is one of the easiest ways to create later tax confusion. - Waiting until after the move to organise the evidence.

The best decisions are often the ones made before UK residence restarts. - Forgetting the claim is source-specific and return-driven.

FIG is not automatic.

Common objections

Objection

“I’ve been in the UAE for years, so I’ll obviously qualify.”

Emotional logic

A long time abroad feels decisive.

Practical risk

A previous UK-resident year, an unexpected tie, or a bad assumption on split-year treatment can break the 10-year condition.

Next step

Map each tax year properly before building a plan around eligibility.

Objection

“If the money is foreign, FIG deals with it.”

Emotional logic

The phrase “foreign income and gains” sounds broad enough to cover everything offshore.

Practical risk

Employment income, disqualified income, and pre-6 April 2025 remittance-basis amounts may need completely different treatment.

Next step

Classify each receipt by source, date and tax character before making any remittance or disposal decision.

Objection

“I’ll sort the tax after I move back.”

Emotional logic

The relocation itself feels more urgent than the tax review.

Practical risk

The best timing opportunities are often lost by the time you become UK resident again.

Next step

Run the planning 6 to 12 months before the move where possible.

Self-diagnostic

Score yourself 1 point for each yes.

Total possible score: 12

- I know the exact tax year in which UK residence is likely to restart.

- I have checked whether I was non-UK resident for the prior 10 consecutive tax years.

- I know whether split-year treatment may matter.

- I can separate old capital from old income and old gains offshore.

- I know whether I ever used the remittance basis before 6 April 2025.

- I know which foreign receipts are investment income and which are employment income.

- I know whether any disposal should happen before UK residence starts.

- I understand what allowances are lost if I claim FIG.

- I know whether ANI issues could affect childcare or Child Benefit positions.

- I know whether OWR needs to be analysed alongside FIG.

- I know whether TRF may be relevant to old offshore funds.

- I have a documented return-to-UK tax plan rather than a rough intention.

Green: 9 to 12

You are thinking about the move in the right sequence.

Amber: 5 to 8

You have part of the picture, but there are likely blind spots that could become expensive.

Red: 0 to 4

You are at real risk of making timing or classification mistakes before you even file the first UK return.

What to check this week if you may return to the UK

- Build a year-by-year residence timeline.

- Identify whether you actually satisfy the 10-year non-residence condition.

- Separate old pre-6 April 2025 offshore funds from new post-2025 income and gains.

- Review likely bonuses, deferred pay, share income and overseas duties separately from investment income.

- Identify any disposals that may need to happen before UK residence restarts.

- Check whether a TRF election could be relevant.

- Make sure the future Self Assessment process will support a clean claim.

This is boring work. It is also the work that usually saves the money.

What happens next

For some people, FIG will be one of the most useful reliefs in the whole return-to-UK process. For others, it will matter, but only as one piece of a bigger puzzle involving split-year treatment, OWR, old remittance-basis funds, property disposals, and family tax thresholds.

The people who usually get the best result are not the people who read the acronym once and assume they are covered. They are the ones who organise the chronology, separate the pots, identify the receipts properly and make deliberate decisions before the move rather than after the tax return deadline has already arrived.

If you are a British expat in the Middle East and a return to the UK is on the horizon, book a return-to-the-UK FIG planning call. The value is rarely in knowing the rule exists. The value is in getting the sequence right.

You may also like

Conclusion

The Foreign Income and Gains regime is one of the most important changes for returning expats, but it is easy to misunderstand if you only read the headline version.

Yes, it can be valuable. Yes, it can create a genuine four-year planning window. But no, it does not cover everything, it does not clean up older offshore issues, and it does not remove the need for disciplined pre-return planning.

The real win is not claiming FIG for the sake of it. The real win is knowing which receipts belong in the claim, which do not, what should happen before UK residence restarts, and how to avoid creating a bigger problem with old offshore funds or employment income on the way back.

That is why the best FIG planning is rarely done after the move. It is done before the plane lands.

If you are planning a move back to the UK and want clarity on whether you qualify for FIG, how it interacts with old offshore funds, and what should be done before your UK residence starts, book a return-to-the-UK tax planning call.

FAQ

Quick definitions

FIG

The post-6 April 2025 UK regime that can relieve eligible foreign income and gains for qualifying new residents.

Qualifying new resident

A person who is UK resident in the relevant tax year and has not been UK resident for at least 10 consecutive tax years immediately before that year, subject to the statutory conditions.

TRF

The Temporary Repatriation Facility for certain pre-6 April 2025 foreign income and gains of former remittance basis users.

OWR

Overseas Workday Relief, a separate relief for qualifying foreign employment income under the post-2025 framework.

What is the FIG regime in simple terms?

It is a UK tax relief that can allow qualifying new residents to claim relief on eligible foreign income and gains arising during their first 4 tax years of UK residence. It replaced the remittance basis from 6 April 2025.

Who qualifies for the 4-year FIG regime?

Broadly, someone who is UK resident in the relevant tax year and has not been UK resident for at least 10 consecutive tax years immediately before that year, subject to HMRC’s detailed conditions.

Is the FIG regime automatic?

No. HMRC says you must make the claim through Self Assessment using the residence and FIG pages and the relevant supplementary pages for the income or gains being relieved.

Does FIG cover foreign salary and bonus income?

Not under the FIG foreign income claim itself. HMRC says relevant foreign earnings and foreign specific employment income are not qualifying foreign income for that purpose, though OWR may be relevant.

Do you lose your personal allowance if you claim FIG relief?

Yes. HMRC says a FIG claim means losing the personal allowance and CGT annual exempt amount, along with certain other allowances and tax reductions.

What happens to old offshore income and gains from before 6 April 2025?

They are not automatically relieved by FIG. HMRC says former remittance basis users may need to consider the Temporary Repatriation Facility, which can apply reduced rates to designated pre-6 April 2025 foreign income and gains.

Can British expats in Dubai use the FIG regime when returning to the UK?

Potentially yes, but only if they satisfy the qualifying conditions, especially the 10 consecutive tax years of non-UK residence test. Living in Dubai is not enough on its own.