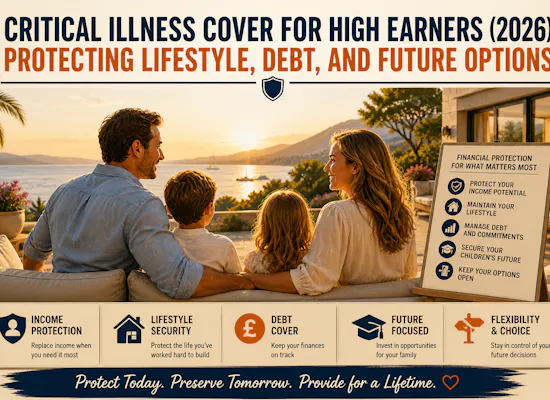

Critical Illness Cover for High Earners: Protecting Lifestyle, Debt, and Future Options

High earners often insure the easy things.

The car.

The house.

The phone.

The watch.

The contents.

But the asset that funds everything else is often underprotected.

Their ability to keep earning.

For many senior professionals, business owners and expats in the Middle East, the real financial risk is not simply dying early.

It is surviving a serious illness, being unable to work properly, and watching the financial plan unravel while life continues.

The mortgage still needs paying.

School fees still arrive.

Rent still needs covering.

Staff may still need paying.

Investment contributions may stop.

Retirement plans may be delayed.

A spouse may need to reduce work.

A business may lose momentum.

And the family may need more flexibility, not less.

That is where critical illness cover can matter.

Not because it solves the medical problem.

It does not.

But because it can provide a tax-free lump sum, depending on jurisdiction and policy structure, at the exact moment when cash, choice and breathing space may matter most.

For high earners, critical illness cover should not be viewed as a small bolt-on to life insurance.

It should be reviewed as part of a wider protection plan covering lifestyle, debt, income, family commitments, business risk and future options.

People also ask

What is critical illness cover?

Critical illness cover is an insurance policy that pays a lump sum if the insured person is diagnosed with a specified serious illness or undergoes a covered medical procedure, subject to the policy terms, definitions, exclusions and survival period.

Is critical illness cover worth it for high earners?

It can be, especially where a serious illness would affect mortgage payments, school fees, family lifestyle, business income, investment contributions or retirement plans. The higher the lifestyle commitment, the more important liquidity can become.

Is critical illness cover the same as income protection?

No. Critical illness cover usually pays a lump sum on diagnosis of a covered condition. Income protection usually pays a regular income if you cannot work because of illness or injury. They solve different problems and may work best together.

How much critical illness cover should a high earner have?

There is no universal number. Cover should usually be linked to debt, income replacement needs, medical and recovery costs, school fees, spouse or family support, business continuity and the amount needed to keep long-term plans on track.

Do expats need critical illness cover?

Expats should review it carefully. Moving abroad can affect employer benefits, access to state support, medical systems, residency, debt, school fees and family support. Existing UK cover should also be checked to confirm whether it remains valid while living overseas.

At a glance

- Critical illness cover is about protecting choices, not just paying bills.

- High earners often have high fixed commitments, including mortgages, school fees, lifestyle costs, staff, debt and family support.

- A serious illness can damage both income and long-term wealth creation.

- Critical illness cover and income protection solve different problems.

- Employer benefits may not be enough, especially for expats, business owners and internationally mobile families.

- The right level of cover should be based on liabilities, income needs, family commitments and future planning goals.

- Policy definitions matter. Not every serious illness will lead to a payout.

- Protection planning should be reviewed alongside pensions, investments, debt, estate planning and business continuity.

The short answer

High earners should consider critical illness cover as part of a wider financial protection plan.

The purpose is not simply to insure against illness.

The purpose is to protect the financial choices that illness can take away.

A well-structured policy can help answer practical questions such as:

- How would the mortgage be paid?

- Could school fees continue?

- Would my spouse need to stop work?

- Could I take time away from the business?

- Would I need to draw from investments at the wrong time?

- Would retirement contributions stop?

- Would I need private treatment or recovery support?

- Would my family have enough liquidity?

- Could I change career if I could not return to the same role?

For high earners, the problem is rarely just survival.

It is maintaining control when income, health and time are suddenly uncertain.

Why high earners underestimate critical illness risk

High earners often have strong cash flow.

That can create a false sense of security.

When income is high, most financial problems feel manageable.

If the mortgage is large, the income covers it.

If school fees rise, the bonus absorbs it.

If investments fall, future earnings can rebuild the portfolio.

If spending is high, cash flow hides the pressure.

But that only works while income continues.

A serious illness can attack the financial plan from several angles at once:

- income may reduce or stop

- bonuses may disappear

- business profits may fall

- medical and recovery costs may rise

- a spouse may need to reduce work

- childcare or home support costs may increase

- investments may be accessed early

- retirement contributions may pause

- debt may become harder to service

This is why protection planning is not about pessimism.

It is about financial resilience.

The Association of British Insurers reported that UK insurers paid a record £8 billion in protection claims during 2024. Individual critical illness payouts rose to £1.3 billion, with the average claim paid at £67,600. Cancer remained the most common reason for a critical illness payout, representing 62% of claims paid.

That does not mean every policy pays.

It does not mean every illness is covered.

But it does show why critical illness cover exists.

When the event happens, the money can matter.

The real issue is not just medical cost

Many high earners focus on medical insurance.

That is important.

But medical insurance and critical illness cover do different jobs.

Medical insurance may help pay for diagnosis, treatment, hospital care, consultations and related medical bills, depending on the policy.

Critical illness cover pays money to you, if the claim meets the policy conditions.

That lump sum can then be used however you choose.

For example:

- repay debt

- replace lost income

- cover school fees

- fund recovery time

- pay for home help

- adapt a property

- allow a spouse to stop working temporarily

- support children

- protect investments from forced selling

- keep retirement plans on track

- buy time to make better decisions

This flexibility is the point.

A serious illness does not only create medical bills.

It creates life disruption.

Critical illness cover helps protect against the financial consequences of that disruption.

Critical illness cover versus income protection

Critical illness cover and income protection are often confused.

They are not the same.

Critical illness cover

Critical illness cover usually pays a lump sum if you are diagnosed with one of the specified conditions in the policy and meet the definition.

It is useful for:

- repaying debt

- creating immediate liquidity

- covering large one-off costs

- funding treatment or recovery flexibility

- reducing financial pressure quickly

- giving the family breathing space

Income protection

Income protection usually pays a regular income if you are unable to work because of illness or injury, subject to the policy terms.

It is useful for:

- replacing monthly income

- covering ongoing living costs

- maintaining family lifestyle

- protecting retirement contributions

- reducing the need to use savings

- supporting long-term incapacity

For many high earners, this is not an either-or decision.

The two policies solve different problems.

A serious illness may create both:

- an immediate need for capital

- an ongoing need for income

Critical illness cover can provide capital.

Income protection can provide income.

Together, they can form a more complete protection strategy.

Why employer benefits may not be enough

Many high earners assume their employer benefits cover the problem.

Sometimes they help.

But they may not be enough.

Employer benefits might include:

- death in service

- private medical insurance

- group income protection

- group critical illness cover

- sick pay

- discretionary bonus continuation

- employee assistance support

These can be valuable.

But they need to be tested.

Key questions include:

- What exactly is covered?

- How much is covered?

- How long does sick pay last?

- Is bonus income included?

- Are allowances included?

- Does the cover continue if you leave?

- Does it apply if you move country?

- Are pre-existing conditions excluded?

- Are children or spouses covered?

- Is the benefit taxable?

- Does the cover match your liabilities?

The issue for high earners is that employer benefits often protect a standard version of life.

But high earners may have a more complex version:

- higher mortgages

- international school fees

- dependants in multiple countries

- business interests

- property overseas

- investment commitments

- lifestyle costs

- future retirement plans

- income based on bonuses or carried interest

A group policy may be helpful.

But it may not be enough to protect the whole financial picture.

The expat problem

For expats, protection planning can become more complicated.

A British expat in Dubai, Abu Dhabi, Riyadh, Doha, Manama, Muscat or Kuwait may have:

- income in AED, SAR, QAR, BHD, OMR or KWD

- UK pensions

- UK property

- offshore investments

- school fees in the Gulf

- medical insurance through an employer

- life cover from a UK provider

- family in another country

- plans to retire elsewhere

- liabilities in more than one currency

That creates practical questions.

Does your existing UK policy remain valid while living abroad?

Would a claim be paid if you are resident overseas?

Is your occupation or location accepted by the insurer?

Are premiums paid from the correct account?

Is the benefit payable in the right currency?

Does the policy cover your current role and travel pattern?

Would your spouse know who to contact?

Would local medical evidence be accepted?

Could a policy lapse if your bank account changes?

These are not small administrative issues.

They are the difference between having cover and thinking you have cover.

For expats, protection planning should be reviewed when you move country, change employer, take on debt, have children, start a business, change residency or revise retirement plans.

What critical illness cover protects for high earners

The better way to think about cover is not:

How much insurance do I need?

It is:

Which financial decisions would I want to protect if I became seriously ill?

Lifestyle

High earners often have high fixed costs.

That may include:

- rent or mortgage payments

- school fees

- domestic staff

- travel

- family support

- car finance

- club memberships

- regular savings

- investment contributions

- property costs

Some of those costs can be reduced.

Some cannot.

Critical illness cover can help provide time to adjust without forcing rushed decisions.

Debt

Debt is one of the clearest reasons to consider cover.

This may include:

- residential mortgage

- investment property debt

- business loans

- personal loans

- director guarantees

- education loans

- credit facilities

A serious illness can make debt feel much heavier.

A lump sum may allow the family to reduce or clear liabilities, depending on the policy level.

School fees

For expat families, school fees are often one of the largest financial commitments.

If a parent becomes seriously ill, the family may still want children to remain in the same school.

That can be emotionally and practically important.

Cover can help preserve continuity.

Future options

This is the most overlooked point.

Critical illness cover is not just about maintaining the current lifestyle.

It is about protecting future options.

For example:

- taking a year out to recover

- reducing working hours

- changing career

- selling a business more slowly

- avoiding forced asset sales

- delaying retirement withdrawals

- funding specialist care

- allowing a spouse to pause work

- keeping children’s education plans intact

High earners often value control.

Critical illness cover protects control when health removes certainty.

How much cover should a high earner consider?

There is no universal formula.

A useful starting point is to split the need into five buckets.

1. Debt clearance

How much debt would you want cleared or reduced?

This might include:

- mortgage

- investment property debt

- personal loans

- business debt personally guaranteed

- school fee commitments

2. Lifestyle runway

How much cash would the family need for 12, 24 or 36 months?

This should include:

- living costs

- rent or mortgage

- school fees

- healthcare gaps

- travel

- home help

- childcare

- spouse income reduction

3. Recovery and treatment flexibility

Would you want funds available for:

- private treatment

- second opinions

- overseas treatment

- rehabilitation

- home adaptations

- recovery time

- specialist support

4. Wealth-building protection

How much would be needed to keep long-term goals on track?

This may include:

- pension contributions

- investment contributions

- education funding

- business continuity

- retirement gap funding

5. Family and business continuity

Would illness affect:

- business revenue

- key person value

- shareholder obligations

- staff costs

- family dependants

- succession planning

The right amount of critical illness cover should reflect the actual financial shock you are trying to protect against.

For high earners, that number may be materially higher than a basic mortgage-linked policy.

Five worked examples with numbers

Example 1: Senior executive with large mortgage and school fees

James is 45, lives in Dubai and earns AED 90,000 per month.

He has:

- £850,000 UK mortgage

- AED 180,000 annual school fees

- AED 70,000 monthly household spending

- £400,000 in pensions

- $250,000 in investments

- limited personal critical illness cover

If James suffers a covered critical illness, the financial issue is not just medical treatment.

The family may need:

- debt reduction

- two years of lifestyle support

- school fee continuity

- time for James to recover

- flexibility for his spouse

A basic £100,000 policy may not be enough.

The planning conversation might consider a much larger lump sum, potentially alongside income protection, life cover and emergency cash.

Example 2: Business owner whose income depends on the company

Sarah owns a profitable UAE business.

She takes:

- AED 65,000 per month from the company

- occasional dividends

- no formal sick pay

- limited retained personal investments

If she becomes seriously ill, the company may suffer at the same time her household income falls.

That is a double risk.

Critical illness cover may help provide personal liquidity, but the business may also need key person cover, shareholder protection or business continuity planning.

The question is not just:

What does Sarah need personally?

It is also:

What happens to the business if Sarah cannot work?

Example 3: Banker with bonus-dependent lifestyle

Michael earns a strong base salary but relies on annual bonuses for:

- pension contributions

- investment top-ups

- school fees

- mortgage overpayments

- family travel

- future retirement planning

A serious illness may not stop all income immediately.

But it may stop bonuses.

That matters.

If Michael’s long-term plan depends on bonuses continuing for the next ten years, critical illness planning should consider not just current bills but missed future wealth accumulation.

Example 4: Expat couple with one main earner

Tom and Priya live in Abu Dhabi with two children.

Tom earns most of the household income.

Priya works part-time and manages much of the family’s day-to-day life.

If Tom becomes seriously ill, Priya may need to reduce or stop work, manage care, support the children and coordinate treatment.

The financial need includes:

- lost income

- additional childcare

- school continuity

- family travel

- domestic support

- emotional breathing space

This is where critical illness cover can protect the whole family system, not just one person’s salary.

Example 5: High earner approaching retirement

David is 57 and plans to retire at 62.

He has:

- £1.2 million in pensions and investments

- £300,000 mortgage

- adult children still partly financially dependent

- no critical illness cover

- strong income for the next five years

His plan works if he keeps earning until 62.

But if a serious illness stops work at 57, the plan changes.

He may need to draw from investments earlier, pause contributions, clear debt or reduce lifestyle.

That creates sequence of returns risk and retirement timing risk.

For near-retirees, critical illness cover can protect the final stretch before financial independence.

Self-diagnostic: is your protection plan strong enough?

Score one point for each “yes”.

- I know exactly what my employer would pay if I became seriously ill.

- I know whether my bonus, allowances or variable income are protected.

- I have checked whether my existing cover remains valid while living abroad.

- I know how much debt I would want cleared if I became critically ill.

- I have calculated how many months of lifestyle costs my family could cover.

- School fees or children’s costs are included in my protection planning.

- I have reviewed critical illness cover separately from life insurance.

- I understand the difference between critical illness cover and income protection.

- I know whether my spouse or partner could maintain the household financially.

- My business or employer dependency risk has been reviewed.

- I have checked policy definitions, exclusions and survival periods.

- My protection plan has been reviewed in the last two years.

Green: 9 to 12 points

Your protection planning may be reasonably well structured, although it should still be reviewed regularly and after major life changes.

Amber: 5 to 8 points

There may be gaps. You should review critical illness cover, income protection, life cover, employer benefits and liquidity together.

Red: 0 to 4 points

Your family or business may be heavily exposed if serious illness affects your income. This should be reviewed as a priority.

Common mistakes

Assuming medical insurance is enough

Problem

Medical insurance may cover treatment costs, but not lost income, debt, school fees or lifestyle commitments.

Why it matters

A serious illness creates financial disruption beyond hospital bills.

What to check

Review critical illness, income protection, emergency cash and debt cover together.

Only insuring the mortgage

Problem

Many people set cover equal to mortgage debt only.

Why it matters

High earners often have large non-mortgage commitments, including school fees, lifestyle costs and investment contributions.

What to check

Calculate the full financial shock, not just the debt.

Confusing critical illness cover with income protection

Problem

A lump sum and a monthly income solve different problems.

Why it matters

You may need both immediate capital and ongoing income support.

What to check

Review how the policies would work together.

Ignoring policy definitions

Problem

People assume every serious illness is covered.

Why it matters

Claims depend on policy definitions, severity, exclusions and survival periods.

What to check

Review the actual wording, not just the headline list of illnesses.

Leaving cover behind when moving abroad

Problem

An expat may assume an old UK policy still works exactly as intended.

Why it matters

Residency, occupation, travel, premium payment and claims evidence can all matter.

What to check

Confirm ongoing validity with the provider or adviser.

What high earners should review now

Employer benefits

Ask for a full benefits schedule.

Check:

- sick pay

- group income protection

- group critical illness cover

- death in service

- private medical insurance

- whether bonus income is covered

- whether benefits continue after leaving employment

Personal policies

List every policy you own.

Include:

- life insurance

- critical illness cover

- income protection

- mortgage protection

- business protection

- key person cover

- shareholder protection

- children’s critical illness benefits

Debt and liabilities

Review what you would want cleared, reduced or protected.

Include:

- mortgages

- property loans

- personal loans

- director guarantees

- school fee commitments

- business debt

- family support

Monthly lifestyle costs

Calculate your true monthly household cost.

Include:

- housing

- schooling

- food

- travel

- transport

- utilities

- insurance

- domestic staff

- family support

- investment contributions

Future options

Ask what you would want the money to make possible.

For example:

- time off work

- treatment flexibility

- career change

- business transition

- spouse support

- children’s continuity

- retirement plan protection

Common objections

“I already have life insurance.”

Emotional logic

Life insurance feels like the main protection product.

Practical risk

Life insurance usually pays on death or terminal illness. It may not help if you survive a serious illness but cannot work or need major lifestyle changes.

Next step

Review life cover, critical illness cover and income protection as separate needs.

“My employer covers me.”

Emotional logic

A corporate benefits package feels comprehensive.

Practical risk

Employer benefits may be limited, may not include bonus income, and may disappear if you leave employment.

Next step

Ask for the exact benefit schedule and test it against your real household commitments.

“I have enough savings.”

Emotional logic

Cash and investments feel like a flexible safety net.

Practical risk

Using investments after a serious illness may interrupt retirement planning, trigger tax, crystallise losses or reduce future options.

Next step

Decide which risks should be insured and which should be self-funded.

“Critical illness cover is expensive.”

Emotional logic

The premium feels like a visible cost for an event that may never happen.

Practical risk

The cost of no cover may be much higher if illness affects income, debt, school fees and retirement plans.

Next step

Review different cover levels, terms, structures and priorities rather than dismissing the idea completely.

“I am healthy.”

Emotional logic

Current health makes future illness feel unlikely.

Practical risk

Insurance is usually easiest to arrange before health changes.

Next step

Review cover while you are still insurable.

What happens next

Clarify the financial risk

Identify what would actually be at risk if you became seriously ill: debt, income, school fees, business value, retirement plans and family lifestyle.

Review existing protection

Gather employer benefits, personal policies, medical insurance, life cover and income protection details.

Calculate the lump sum need

Work out how much capital would be needed to reduce debt, fund recovery time, protect lifestyle and preserve future options.

Compare critical illness with income protection

Decide which risks need lump sum cover, which need monthly income support and which can be self-funded.

Check expat validity

Confirm that existing policies remain suitable while you live and work overseas.

Document the plan

Make sure your spouse, partner or trusted family member knows what cover exists, who to contact and where the policy documents are held.

You may also like

- Premium Financing vs Paying Cash (2026) for HNW Clients

- How Business Owners Should Value Their Business for Retirement Planning

- How to Build a Globally Mobile Portfolio in 2026

- UK Pensions and Estate Planning: Aligning Beneficiaries With Wills and Trusts

- How Probate Works with Assets in Multiple Countries

Conclusion

Critical illness cover is not just about illness.

For high earners, it is about protecting lifestyle, debt, family stability and future options.

The question is not simply:

Could I survive a serious illness?

The better question is:

Would my financial plan survive one?

If a serious illness would force you to sell investments, stop school fees, delay retirement, rely on your spouse, sell a business quickly or reduce your family’s options, the protection plan may need reviewing.

Medical insurance may help with treatment.

Life insurance may help if you die.

Income protection may help if you cannot work.

Critical illness cover can help provide capital while you are still alive and facing some of the hardest decisions your family may ever make.

If you are a high earner and you are not sure whether your critical illness cover, income protection, life cover and wider financial plan are properly aligned, book an introductory call with Josh Clancey.

FAQ

Quick definitions

Critical illness cover

Insurance that usually pays a lump sum if you are diagnosed with a covered serious illness or undergo a covered procedure, subject to the policy terms.

Income protection

Insurance that usually pays a regular income if you cannot work because of illness or injury, subject to the policy terms.

Life insurance

Insurance that pays a lump sum or benefit on death, and sometimes terminal illness, depending on the policy.

Survival period

The period you must survive after diagnosis or surgery before a critical illness claim is payable.

Exclusion

A condition or circumstance that is not covered by the policy.

Is critical illness cover worth it?

It can be worth considering if a serious illness would affect your income, mortgage, school fees, business, retirement plan or family lifestyle.

What illnesses are covered?

Policies vary. Common covered conditions may include certain cancers, heart attacks, strokes and other specified illnesses or procedures. The exact definitions matter.

Does critical illness cover pay if I cannot work?

It pays if you meet the policy definition for a covered condition, not simply because you cannot work. Income protection is usually designed to address inability to work.

How much cover do I need?

The amount should be based on debt, lifestyle costs, school fees, recovery needs, income replacement, business risk and long-term financial goals.

Should I have critical illness cover and income protection?

Many high earners should review both. Critical illness cover provides capital. Income protection provides ongoing income. They solve different problems.

Does critical illness cover apply to expats?

It depends on the policy. Expats should check residency, travel, occupation, claims evidence, currency and premium payment rules.

Is employer critical illness cover enough?

It may help, but it may not be enough. Employer benefits can be limited and may end when employment ends.

Can business owners get critical illness cover?

Yes, but business owners should also consider key person cover, shareholder protection, business debt and succession planning.

Does critical illness cover replace medical insurance?

No. Medical insurance helps cover treatment costs. Critical illness cover provides a lump sum if the policy conditions are met.